$DDI – Doubledown Interactive Inc (English version)

$DDI – Doubledown Interactive Inc (English version)

LONG | Mobile gaming company | Net Cash | EV/EBITDA = 4x | Founder/CEO with skin in the game | 80%-120% upside|

1. ABOUT THE COMPANY

DoubleDown Interactive Co Ltd (SDDI) is a company based in South Korea that develops and publishes digital games on mobile and web platforms. The main theme of their games is Social Casino, being their flagship "DoubleDown Casino", although they are developing "casual" games in search of diversification as we will see below.

DoubleDown was established in 2008 as "The8Games Co Ltd" and changed its name to its current name in 2019 when it became part of DoubleU Games Co Ltd. DoubleDown Interactive Co Ltd operates as a subsidiary of DoubleU Games Co Ltd (hereinafter DUG), a South Korean listed company (ticker: 192080.KS) also engaged in the development of games for mobile and web enabled platforms.

On September 1, 2021, DoubleDown was listed on the NASDAQ under the ticker DDI.

2. BUSINESS MODEL - GAMES

DoubleDown games operate on a "Free-to-Play" model, whereby players can collect virtual currency (hereafter "chips") in the in-game store or in-game promotions. The virtual currency helps you advance in the game, obtaining new levels that in turn help you earn more chips. In addition, some games have a subscription model that allows you to earn chips more quickly. The second way of earning is advertising in some of their applications.

The main theme is social casino, i.e. slots games, roulette, bingo, jackpot, etc.

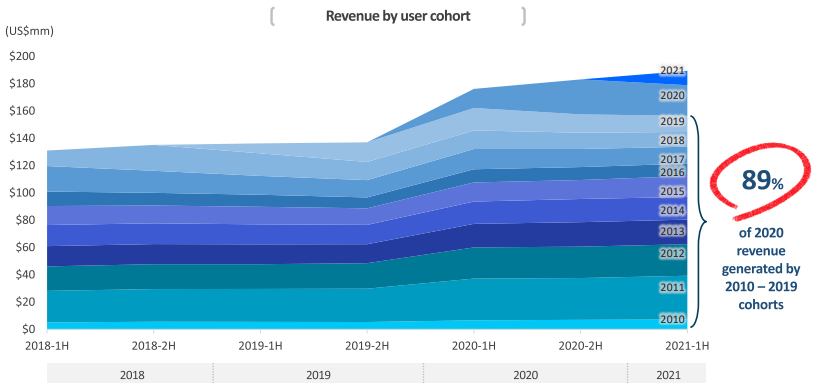

The key to the business model is the ability to acquire, retain and monetize players over time. In 2020, 89% of its sales were generated by users who installed the app in the period 2010-2019.

Currently, there are 5 Doubledown games available on the main mobile platforms (Apple and Google) although they can also be played through Facebook and web platform:

-DoubleDown Casino is undoubtedly the most important game for the Company. The game replicates the Vegas ecosystem with games such as slots, roulette, jackpot, bingo, etc. It was launched in 2010 on Facebook, obtaining in only 23 months more than 10 million downloads. In 2012, it was launched in Google Play, Apple Store and Amazon Appstore. In 2021, the game has more than 250 fee-to-play slots. According to the specialized gaming agency Eilers & Krejcik, DDCasino was the Top 3 games by revenue in 2020.

- DoubleDown Fort Knox, launched in 2018, is available only for mobile platforms on Apple Store and Google Play. This Game like DoubleDown Casino is based on slots, bingo and roulette mainly, but it is more focused on a young audience, with a better defined and immersive platform.

- DoubleDown Classic, launched in 2017, is a slots game with a classic old-fashioned interface. It is available on Apple Store and Google Play.

- Ellen's Road to Riches, launched in 2017, is a social casino game based on the content of the famous American TV show: "The Ellen DeGeneres Show". It can be played both on web and mobile (Apple Store, Google Play and Amazon Appstore).

Since the end of 2020, they have been developing games outside the Slots area, wanting to expand into casual games to diversify their product portfolio. In 2021, the beta of the company's first casual game was launched: Undead World: Hero Survival, a free-to-play RPG style game, available both on mobile and web.

In addition, a new space-themed social casino, Project G, is expected to be launched in early 2022.

3. MANAGEMENT / OWNERSHIP

To talk about DoubleDown Casino's management, we must start by talking about DoubleU Games, the parent company domiciled in South Korea, which owns 67% of the company's shares (the image below is the pre-IPO situation). As for the IPO process, you can find more info on their website.

DUG has the decision-making power over DDI. So much so that the CEO of the parent company (DUG) is Kim Ga-Ram himself, who is also the founder and largest shareholder of DUG with 40% of the shares. In addition, DUG has been assiduous in share buybacks in the past, holding 7.6% of its own shares. Until the IPO, Kim Ga-Ram was also the CEO of DDI, but he was replaced by Kim In Keuk. Despite this change, decision-making power remains with the founder, CEO and largest shareholder of DUG: Kim Ga-Ram.

Majority shareholders (DUG):

Other DDI shareholders:

Kim Ga-Ram is a 44-year-old electrical engineer with a degree from the Korea Advanced Institute of Science and Technology. Before founding DUG, he worked at Innogrid, a company specialized in Clouding. In 2013, he founded AFewGoodSoft after raising $80 million in a funding round. It would later change its name to DoubleU Games. In February 2017, Kim was ranked the 92nd richest person in Korea. Other than this information, there are not many interviews and articles about Kim Ga-Ram.

4. INDUSTRY / PEERS

Technology and consumer trends mean that the mobile gaming sector will grow considerably in the coming years. According to eMarketer, American adults spend an average of 4.5 hours a day watching a smartphone (excluding calls). In 2020, time spent watching content via mobile was greater than time spent watching TV for the first time in history.

The "social casino" gaming subsector, according to Eilers & Krejcik, is expected to grow by 4.2% annually until 2025. The "casual gaming" sector is estimated to grow by 25% until 2025, according to the same company.

DoubleDown's main competitors are Sciplay ($SCPL), Playstudios ($MYPS), Zynga ($ZNGA) and Playtika ($PLTK). All of them are very focused on the development of slots and casino games, although, like DDI, they are seeking to diversify their portfolio with casual games. Other larger players such as Tencent ($TCEHY), Aristocrat ($ALL.AX), Activision ($ACTVI), etc. should also be added.

To make an objective comparison of the different peers, it is necessary to explain some operational metrics used in this sector.

-ARPDAU ($): Average Revenue per Daily Active User

-AMRPPU ($): Average Monthly Revenue per Paying User

-Payer Conversion rate (%): percentage of users who make purchases compared to the total number of users.

-Average DAU (thousands): Daily Active Users

-Average MAU (thousands): Monthly Active Users

Below is a comparison of the following KPIs:

5. FINANCIALS / VALUATION

DoubleDown has a fairly solid and healthy balance sheet. Its low debt means that at the end of Q3 2021 it will have net cash:

As for the valuation, the method used has been a comparison of multiples with its peers. Although I always like to make a DCF, in this case, being a company whose growth will be mainly due to M&A transactions, it is difficult to estimate its revenues without information on these deals. Below is a table with the main ratios (NTM information from 12/28/2020 obtained from TIKR, the DUG information is from Market Screener):

Taking the average EV/EBITDA ratio of the sector around 8x, we could estimate a target price for DDI of between $25 - $31/share. This would represent an approximate 80% - 120% appreciation from its current price of $14.44/share (12/28/2020 data).

The investment idea itself is highly dependent on what DDI will do with the accumulated cash. In the Q3 2021 conference call management says they want to use that cash to acquire other companies, but if they don't find anything that fits their intentions, they will use it for shareholder remuneration. In my opinion I would bet more on the first one, I think they know that the only option to grow is to buy a company dedicated to casual gaming, the pillar of their strategy for the coming years.

In any case, DDI trades cheap against its peers with only its current business more focused on social casino. This business is already profitable, with good margins and metrics, so assuming that the market values this business like its peers it should already be profitable.

The question then would be, why is it cheap? The main reasons are:

- IPOs have been very punished at the listing level at the end of 2021 unlike in previous years.

- DDI like the rest of the companies in the sector, are coming from a year (2020) very good for the business and the 2021 results are obviously being worse in comparison.

- It is an unknown company, there are only 2 analysts behind the company and none from a Bank or Investment Fund of "the big ones".

- South Korean company with a complex structure, whose parent company does not have all the information available in English.

6. RISKS

- Despite being a sector with good prospects for future growth, there is a lot of competition. There are larger players with greater capacity for innovation. In addition, these players have a larger marketing budget, which allows them to reach a wider audience.

-One of DDI's biggest problems is its concentration in the source of its sales, being very dependent on its flagship game "DoubleDown Casino", which accounts for 95% of its total revenues:

- There is a regulatory risk especially in certain U.S. states that want to restrict mobile gambling and casino games. DDI has had some cases (Benson Case) in which it has been harmed by these regulations.

- Another considerable risk is Apple's new policy related to its IDFA (Identifier for Advertisers). In the new iOs 14 update, users will be able to choose whether or not to give their personal data to app advertisers. This may affect sales from in-game advertising. In addition, Apple is the most important revenue stream for DDI:

- Finally, as we have highlighted above, DDI's strategy for continued growth is based on company acquisitions. This can be an opportunity if good deals are made, but it can also be a complete disaster if it is overpaid. We will certainly have to keep an eye out for more news.

7. CONCLUSIONS

- Good exposure to a consolidated sector with good margins (Casino gaming) and the possibility of growth in the casual gaming sector with future M&A transactions.

-DDI trades at a significant discount to its peers. Its operating ratios are also better than the sector average.

-Company with great growth opportunities through M&A transactions and expansion into new markets through the translation of its games into other languages (Spanish, Mandarin Chinese, French, etc.).

-Possible "play" from its parent company DoubleU Games. Through it, you can reduce the risk of concentration of games with exposure to revenues through more games besides those of DDi. In addition, DoubleU Games pays a dividend. On the downside, there is a lot of information in Korean that is not translated into English.

- Another company in the sector is Sciplay ($SCPL), of which I will surely make an analysis in the next week (Subscribe to not miss it!).

8. SOURCES

https://ir.doubledowninteractive.com/

https://www.doubleugames.com/ir/data.php

https://www.marketresearchfuture.com/reports/mobile-gambling-market-5142

https://app.tikr.com/stock/about?cid=432042767&tid=671564369&ref=2hmlpx

https://www.casino.org/news/doubledown-stock-has-makings-of-social-casino-winner-says-analyst/

https://www.casino.org/news/piaytika-is-buying-reworks-for-600-million-to-expand-app-biz/

https://www.casino.org/news/playstudios-one-of-worst-de-spaced-stocks-of-past-year/

9. DISCLOSURE

As of today (12/28/2021), this company represents a small percentage of my portfolio (<5%). I have written this article on my own and it expresses my opinions. I have received no compensation for it. I have no relationship with this company or any of the companies mentioned in the article. The financial information has been obtained from different sources such as TIKR, Market Screener, the annual accounts of the different companies mentioned, etc. Finally, this article is not a buy recommendation. For any questions or queries:

-Mail: pharomvalue@gmail.com

-Twitter: @PharomValue